Last week, in my “what if” post, I talked about deferred annuity contracts that included chronic illness & nursing home benefit access riders. I want to explain why I have a concern about the use of these riders with annuities (as well as life insurance policies).

It really comes down to this – too often, they are misunderstood by the client and considered a LONG-TERM CARE strategy. They are not long-term care insurance! This comes down to how those policies are classified – long-term care is defined in 7702(b) of IRC while chronic illness is 101(g).

On top of that, 101(g) riders are not allowed to be promoted as long-term insurance – it’s written in the code! AND, it is written in the policy language!

Let’s go back to the “what if” discussion.

“What if” Mrs. Client owns an annuity that she thinks is her long-term care solution and it’s not?

“What if” she owns an annuity that “waives charges” for chronic illness or nursing home and

- receives care at home, or

- is in an assisted living facility, or

- is diagnosed with dementia

- doesn’t meet the company’s criteria for eligibility?

If she qualifies, then surrender charges would be waived for her withdrawal from the annuity and that is it. She can get her money without paying a charge, but the gains will be taxed as ordinary income.

Remember, her annuity was Annuity Care or Indexed Annuity Care provide distributions tax-free for any of these scenarios.

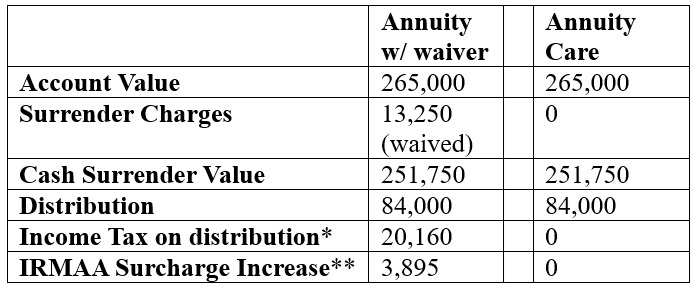

Let’s say that in year 5 of her annuity which has a 9 year surrender, she a health situation that would allow her to meet the criteria to waive charges … here is how it would look if she required $7,000 for 12 months ($84,000 annual).

*assumes resident state of NH and in the 24% tax bracket with an annual adjusted gross income before distribution of $105,000 and filing individual.

** Income Related Monthly Adjustment Amount for Medicare Parts B & D in 2028 assuming modified AGI of $189,000 in 2026 (See cms.gov) – this may be able to be lowered using a combination of accounting and insurance strategies

Remember this … waiving the charges does not significantly impact distribution if they are made outside of the surrender period. They are still a taxable event which may triggers other issues with means tested benefits and programs.

AND, remember this, each company has a different interpretation for what is a triggering event. One may be 2 of 6 activities of daily living as a trigger but for nursing home care only. Another may be 2 of 6 activities of daily living or a cognitive diagnosis as a trigger. It varies by carrier.

Annuity Care or Indexed Annuity Care pay tax-free benefits for long-term care support & services that are triggered by either an inability to perform 2 of 6 ADLs or a cognitive impairment AND pay regardless of where the care is received (at home or in a facility).

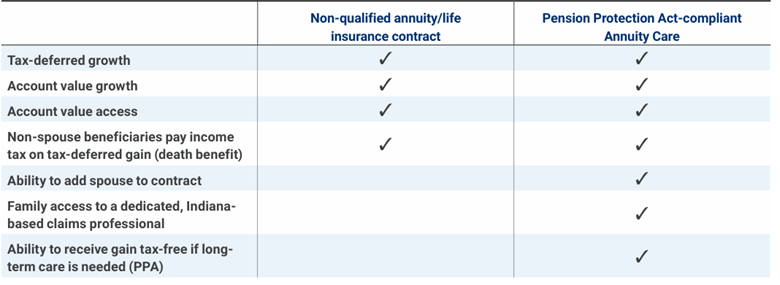

Another way to visualize what I just said is this:

As I said last week, “what if” matters.

“What if” your client plans on using their annuity money as their LTC funding strategy. What is the right place?

Leave a comment