Earlier this week, I had several meetings where I shared the annuity exchange strategy with advisors. It’s something that I’ve been talking about for over a year; yet most have not picked up on the idea.

UNTIL RECENTLY ….

As a refresher, this strategy has unlocked millions of dollars for people when they require funding for long-term care support & services. And, it is (in some cases) the final major transaction that some advisors have had with their clients. Incidentally, when the strategy is deployed, this can also serve as the first introduction to their family.

Here is a quick summary of the annuity exchange strategy. We are simply transferring money from an existing nonqualified deferred annuity into a new nonqualified deferred annuity that has the ability to provide tax-free resources for long term care.

Until that money is needed for long-term care, it will continue to grow tax-deferred. When it is needed, after a short elimination period, the monies are available tax-free to pay for care received at home or from a facility. If they never need to utilize the money, it will pass to whomever that they designate as their beneficiary – just like any other nonqualified deferred annuity.

Remember, this is a long-term care solution NOT a chronic illness add-on. Care at home and in a facility are included as covered benefits AND the trigger for care is either a cognitive impairment or inability to perform 2 of 6 activities of daily living.

It’s as simple as that … it is a leverage opportunity for people age 87 and younger who own nonqualified deferred annuities. The strategy can be instantly approved for up to $1.5 million when the application is submitted electronically by you.

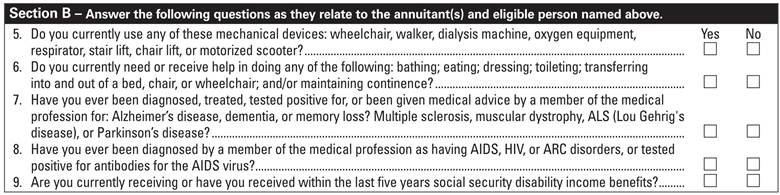

The final caveat is that the client(s) must favorably answer 4 underwriting questions.

Give me a call – let’s talk about your clients’ annuities.

Leave a comment