Earlier this month on LTC Coffee Break, Michael and I discussed true long term care where benefits can last as long as the insured needs them. In a sense, lifetime benefits that cannot be outlived.

Last week, I shared a bit about long duration care events such as Alzheimer’s and Parkinson’s. The impact physically, emotionally, and financially can be staggering – that is why long term care insurance exists to provide a financial resource to pay for high impact healthcare events.

A funny thing long term care – the definition of long term to some is limited or even short duration but rarely push into the traditional investment definitions of long term which can be a decade or more. So, why call it long term care if it really is short term, average, or at best moderate duration? Let’s be honest and call it limited term care.

Consider this, the average duration of care for a man is just under 3 years while a woman is just under 3 ½ years. And, Alzheimer’s is well beyond that – depending upon the information source, 4 to 8 years with cases sometimes lasting two decades.

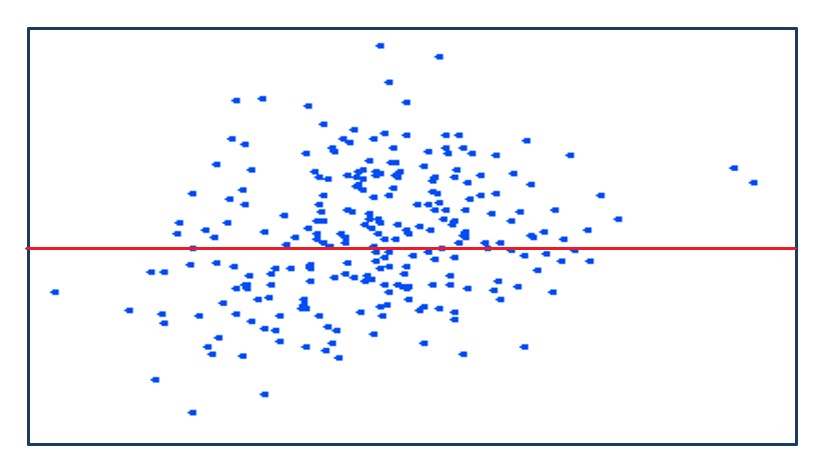

Take a look at this scatter graph.

On it you see 200 data points, the horizontal axis represents cost, the vertical axis is duration, and the line cutting through the middle is the “average” (actually median). If we employ the “average” protection strategy, half of the pool is covered. What about the rest? Are they just out of luck?

If we move that line up to cover double the average, we still leave a chunk of the pool uncovered. Do we tell them that they are out of luck?

Since the purpose for insurance is to mitigate the impact of those high cost long duration situations, why is average acceptable?

My whole point of this whole discussion is to stop leading with average and allowing average to be acceptable.

You must be logged in to post a comment.