A short time ago, I was looking at the Federal Long Term Care Insurance Program website and came across a page dedicated to self-funding.

First off – I was excited that they actually used the terminology self-funding and not “self-insurance”. It is my premise that “self-insurance” in the context of LTC planning is faulty as many advocates of the strategy allow the client to retain all of the risk. Without a transfer of risk or a backstop for catastrophic loss, there is no insurance therefore they are self-funding.

The next point that I thought was solid was a basic discussion of the cost of care. You know it isn’t cheap and we know that people want to stay at home. But, we don’t ever really say that. We paint a picture using national averages for nursing home care.

The cost of care is unique and dynamic based on where someone lives, the type of care, and other factors. Let’s just focus on the cost of care for a moment and compare the CURRENT national average to that of central Connecticut where I live.

| National | Average | Central | CT | |

| Monthly | Annual | Monthly | Annual | |

| Informal Home Care (42 hr/wk) | $6,953 | $83,440 | $7,537 | $90,440 |

| Home Care (42 hr/wk) | $6,535 | $78,421 | $6,061 | $72,733 |

| Assisted Living | $5,862 | $70,349 | $7,454 | $89,443 |

| Nursing Home | $9,619 | $115,428 | $15,292 | $183,508 |

One thing that is deceptive is the cost of informal & formal home care. The number presented are based on 42 hours of services per week (that is 168 hours a 30-day month). There are 168 hours in a week (720 hours in a 30-day month). We can discuss this topic at some other point.

To learn more about the cost in other parts of the country, check out the Interactive Cost-of-Care Map from OneAmerica Financial.

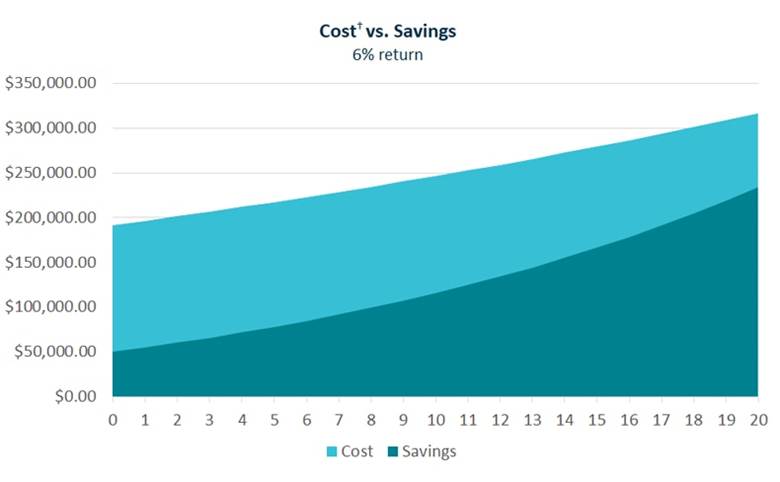

Back to the point – what the website did was present a self-funding strategy along side a cost-of-care assumption over a period of time. The LTC cost was based upon an average the 3 types of care (home, assisted living, nursing home) with an annual inflation rate of 2.54%. They also used a long-term care event lasting 33 month. For the self-funding portion, a 20 year time horizon with $2,000 annually was allocated to the “LTC fund” earning 6% return for a fund that started with $50,000.

Their visual demonstrating the gap looked like this:

The cost represents the 33 months of “average” care. And, as you would expect, it increases year over year. The savings, while growing at a rate of 6% never catches up to the cost during that 20 years despite having $50,000 of seed money.

Think about this for a minute … that is “the plan” that most people accept.

There are plenty of funding alternatives – to learn what OneAmerica Financial can do to improve this situation, contact Kelly Hilliard at (844) 623-2451 or via email at

kelleyhilliard.isp@oneamerica.com

One response to “Can you self-fund?”

The 2.54% inflation rate for the cost of care is ridiculous. That’s the rate for all items, not LTC. I still believe we have to use 5% compound and hope it isn’t more than that. Using the higher inflation rate just makes the comparison that much more compelling. Phyllis Phyllis Shelton Jamison, President

CA license: 0C02572 Got LTCi http://www.GotLTCi.com http://www.gotltci.com/ http://www.gotltci.com/phyllis-shelton/ 615-590-0300 office / 800-582-8425 toll-free 615-590-0307 FAX / 615-406-3908 cell https://calendly.com/phyllis-shelton

LikeLike