Indexed Annuity Care is not intended to replace another annuity product that is intended to generate income. It is designed to provide a protection buffer for other income producing assets.

Like many indexed annuities, Indexed Annuity Care offers upside growth with downside protection while in the accumulation phase BUT it is the ONLY indexed annuity that provides tax-free distributions when used for LTC expenses. The is no other fixed indexed annuity that offers this benefit.

LTC benefits are available when the annuitant must have either a cognitive impairment (like Alzheimer’s, dementia, etc) OR be unable to perform 2 of 6 Activities of Daily Living (bathing, dressing, eating, continence, transferring, or toileting) with a plan of care from a licensed healthcare practitioner. Care can be received at home or a facility.

During the accumulation phase, Indexed Annuity Care will grow in alignment with the accumulation strategy tracking the S&P 500 and calculated using point-to-point or monthly account value average and either a participation rate or cap or by electing for the fixed rate accumulation. (For more specifics, please reference the Indexed Annuity Care Producer Guide).

Remember, the purpose for Indexed Annuity Care is not to make someone wealth – it is to keep them from becoming poor due to an extended healthcare event. With this in mind, Indexed Annuity Care has built in factors to ensure that the pool for LTC benefits will never be less than the initial deposit. (Note: this guarantee is not applicable in Connecticut – Connecticut product variation).

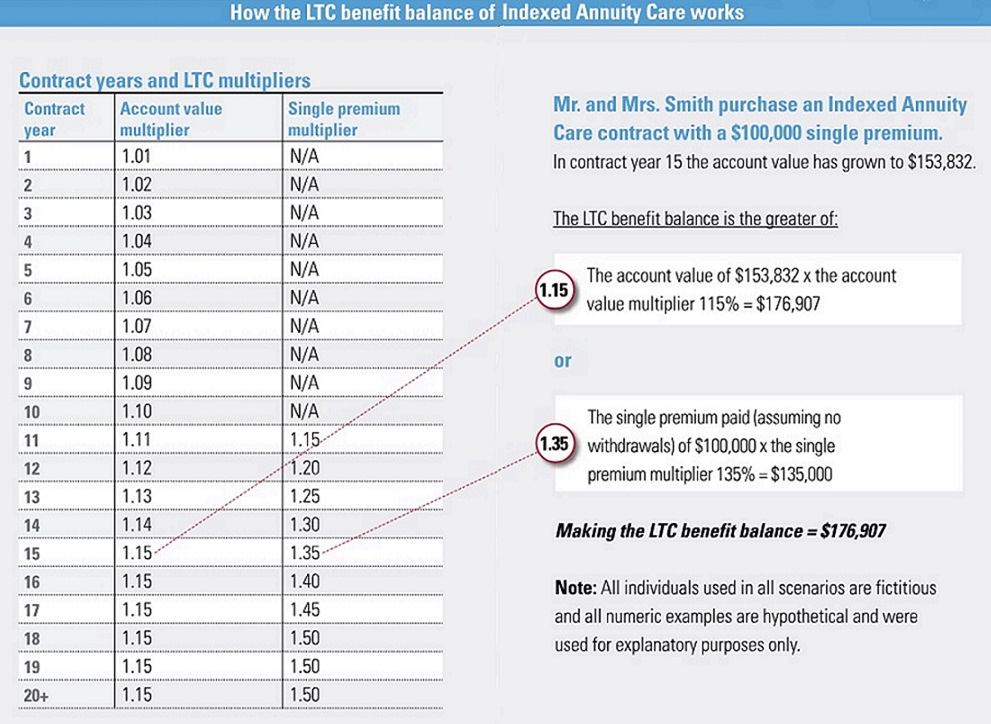

To calculate the monthly benefit, the greater of the account value times the account value multiplier or the initial single premium times the single premium multiplier will be used to calculate the benefit. The example below explains how.

To derive the monthly benefit, simply divide the LTC benefit balance by 30 for a joint policy or 24 for an individual policy. (Yes, Indexed Annuity Care does offer joint benefits for spouses.) In the above scenario, up to $5,897 of tax-free LTC benefits are available.

Even with a zero return, the LTC benefit balance will be greater than the initial premium used to fund the policy. Meaning – the LTC benefit is guaranteed to grow regardless of performance of the underlying annuity.

Note: A Continuation of Benefit Rider (COB) may be added at an additional cost. The can double, triple, or create an unlimited pool of LTC benefits.

You must be logged in to post a comment.