This month, I am sharing a little about funding long term care premiums using qualified money. As a matter of fact, if you want to hear a few ideas, join Michael Florio and me for our LTC Coffee Break on Tuesday mornings at 10am. You can catch our most recent release and access our library of past shows at our website at LTCcoffeebreak.com or just CLICK HERE to begin viewing the video.

For the past 2 weeks, I shared how an inherited IRA can be used to fund Asset Care. I vaguely touched on the workings of the qualified money funding strategy. Today, thanks to a few emails, I will delve into it a bit.

Remember, if you want more information and/or have a specific scenario that you would like to discuss, you can reach out to my internal Justin Fox at (844) 658-3725 or via email at justinfox.isp@oneamerica.com. Of course, I am also available to assist at (678) 512-9627 and at kevin.fisher@oneamerica.com.

Just a reminder, when we are talking about using qualified money, we are talking about non-Roth monies – IRA, 401(k), 403(b), etc. And, we are generally looking for clients aged 59 1/2.

What I am about to share with you is applicable for Asset Care in all states but CA (where the “new” product is not approved) and NY (where OneAmerica does not do business).

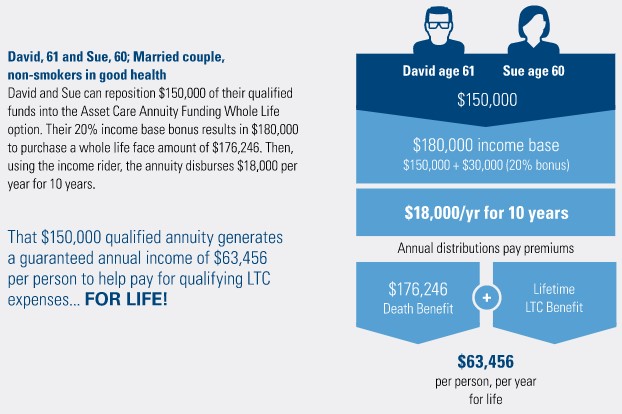

Now, Asset Care funded by qualified money is actually a two stage product. One is the Asset Care policy which can be designed to align with the client’s specific goals and needs in mind. And, the other is a deferred annuity that we will use to hold and distribute the qualified funds.

The annuity portion of the strategy is a deferred fixed annuity with an income rider. This income rider distributes the proceeds over 10 years. Once the proceeds are full distributed, Asset Care is fully funded. Often, I hear “I can do that with a single premium immediate annuity.” Sure, you can do that – BUT, it will take more funds to make that happen.

Once the rollover is received, OneAmerica credits the deferred annuity an additional 20%. This combination of rollover and bonus (which is a guaranteed bonus) will be used to fund the underlying Asset Care policy. Remember, those distributions, since they are qualified money will be taxed as ordinary income.

As I said, every year for 10 years the proceeds from the deferred annuity will be moved into Asset Care providing funding for both the base policy and continuation of benefit rider (COB). Remember, the base policy is a participating whole life policy whose death benefit is accelerated to pay long term care claims until it is exhausted then the COB continues paying the claim until that rider or the claim is exhausted as well.

Here is an example:

One thing to remember here – at OneAmerica, solutions are not cookie cutter and one size fits all. They can be tailored to meet your clients’ specific needs. Long term care solutions with guaranteed premiums and benefits make up the portfolio. And, funding options abound.

Again, if you have any questions, feel free to reach out to either Justin Fox or me.

You must be logged in to post a comment.