Last week, when we were looking at the million and a half of “self-funding”, I shared an idea to improve their “self-funding” strategy. That strategy calls for dedicating a pool of resources specifically for long-term care funding when it is needed.

If you recall, the 70 year old couple had a portfolio comprised of 33.3% stock, 33.3% bonds, and 33.3% annuities where the stock and bond portions are qualified making the distribution fully taxable; the annuity is nonqualified. What I propose as an efficient “self-funding” strategy is to use the Pension Protection Act (PPA) to improve the value of the annuity.

The PPA allows people to transfer the cash value from a life insurance policy or account value from a nonqualified deferred annuity into a PPA compliant annuity which then continues to grow as a deferred annuity but when distributions are made for long-term care support & services, they are tax-free. And, only 4 carriers offer theses products AND annuities that offer income doublers are not PPA compliant.

Remember, the people in this discussion are in their 70s and their nonqualified annuity balance is $500,000. As a reminder, the scenario that play out was for 3 years of home care at $216,720 each year – $650,160 in total. Following the advice of their advisor, they treated the expenses like any other expense and paid from their assets.

So, let’s reposition a portion of that annuity money into a defensive posture using Annuity Care II via 1035 exchange where both spouses have access to the benefits from the policy. Using this strategy, $300,000 produces $10,984 of tax-free LTC benefits that are available for 66 months guaranteed!

This is will be the first money to be used when a long-term care event occurs. It is TAX-FREE which allows the other monies to do what they are best positioned for growth & income.

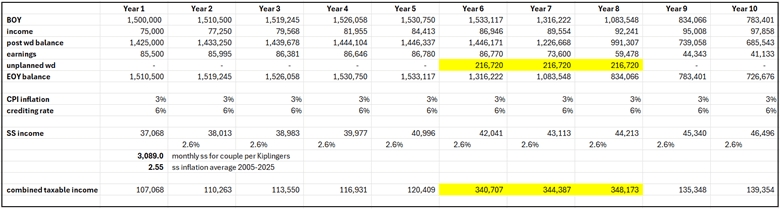

Here you see the impact to taxable income highlighted in yellow of their original strategy:

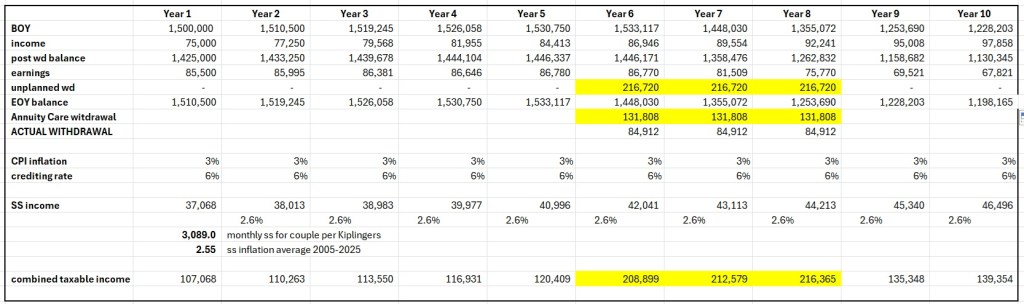

Here is the favorable tax impact of reallocating a portion into an Annuity Care II product where all of the monies for LTC are tax-free:

You will note a couple extra rows. This is simply to demonstrate that a portion of the expenses of $216,720 are self-funded while the other portion is covered by the Annuity Care II benefits. Take note, the combined taxable income in this scenario is lowered. And, you will also note the impact tot he income producing assets is lower.

One last point that is an important one, if you think that the repositioning isn’t that important, it could be. It could keep the couple avoid a situation where the Medicare Income Related Monthly Adjustment Amount (IRMAA) surcharge is triggered. In 2026, that is triggered when a couple’s Adjusted Gross Income is over $206,700 and increases as incomes grow. In this scenario, we are looking out a few years where (in all likelihood) the surcharge would be greater (and remember, it is a lag surcharge meaning that it does not impact you until years following the high income.)

Additionally, in some cases, this simple partially funded insurance strategy can help avoid unnecessary fees and charges for early surrender or liquidations. In short, this simple strategy can put assets in the position where they are most efficient.

One last thought, if they were a little compromised in health and unable to secure an Annuity Care II policy, there are other PPA solutions. And, those solutions are available up to the age of 87!

You must be logged in to post a comment.