So, your advisor tells you that your “$1.5 million is enough to self-insure.”

For over a month, I have challenged that premise using a scenario that represents an average duration situation 10 years in the future using today’s dollars as a cost benchmark. Needless to day, after a 3 year duration situation, the account value (assuming an annual 6% growth) crashed from $1.5 million to $834k.

Imagine what would have happened if they required 6 years of care. Assuming an annual LTC expense of $216,720 – over $1.3 million would have been expended on care. How’s that $1.5 million holding up now? Remember, that annual cost is today’s dollars for 18 hours of care per day.

Our first discussion looked at repositioning a nonqualified deferred annuity into a more favorable liquidation posture. At worst, they pass the annuity to their heirs. At best, they get tax-free benefits from the policy reducing the amount that they liquidate from their accounts AND keep the income tax profile low.

Last week, I shared an idea of using qualified money to leverage into an Asset Care policy. This idea focused on the turn-key solution only available from OneAmerica Financial and Asset Care. Other options exist and I am about to share one with you that might be beneficial to that “self-insurance” believer.

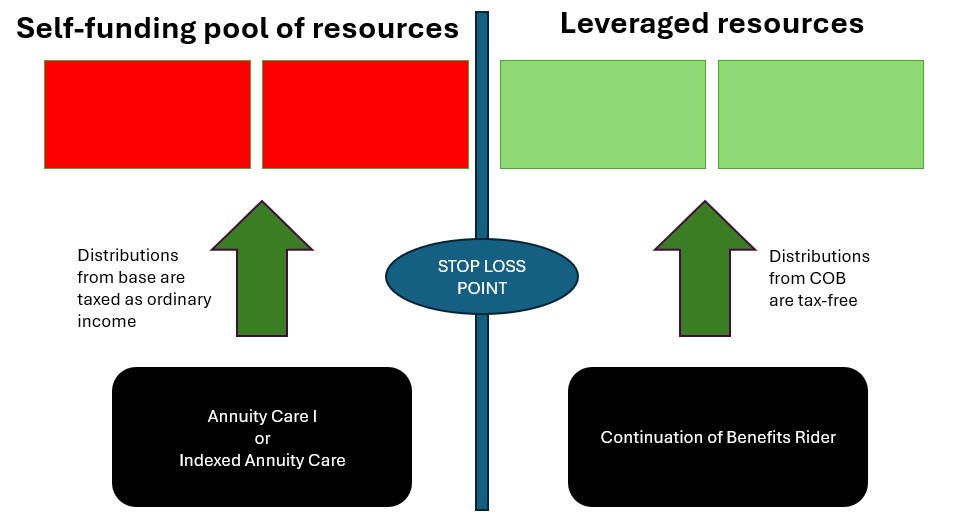

By the way, there is no such thing as “self-insurance”. It is full out risk retention A dollar-for-dollar cost with zero leverage. In order for any form of insurance to be present, there needs to be leverage and a transfer of the risk. It is SELF-FUNDING!

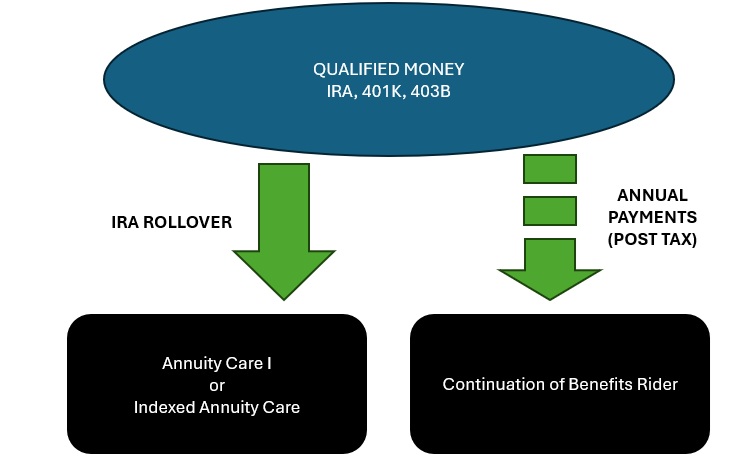

Anyway, here is an idea that you might want to consider. Since we are talking about qualified money, it does not qualify for Pension Protection Act benefits where tax-deferred earnings become tax-free LTC benefits.

HOWEVER, we can devise a plan where we allocate / designate a portion of the qualified money as the LTC fund and pour it into Annuity Care or Indexed Annuity Care. Then out of that qualified money, fund a continuation of benefits rider. Remember, the premiums used to fund the COB may be a deductible LTC premium.

In this scenario, the first couple of years of long term care benefits paid from the Annuity Care policy will be taxed as ordinary income. Once the base annuity is exhausted, then benefits paid from the continuation of benefits rider are paid tax-free! And, remember this you can purchase the COB to be an unlimited stream of benefits.

This is putting a “stop-loss” provision into the self-funding decision.

Let me ask you this, would you rather allocate $300,000 of your monies that will produce a million of tax-free resources for LTC or pay dollar for dollar that $1 million that will never be recovered?

Remember this – with the Annuity Care Continuation of Benefits, that stop-loss point can be a bucket similar to the self-funded pool or an unlimited stream of money.

To learn more about using qualified money with Annuity Care products, give me a call.

Leave a comment