A question that occasionally comes up is can I use qualified money with a product like Annuity Care?

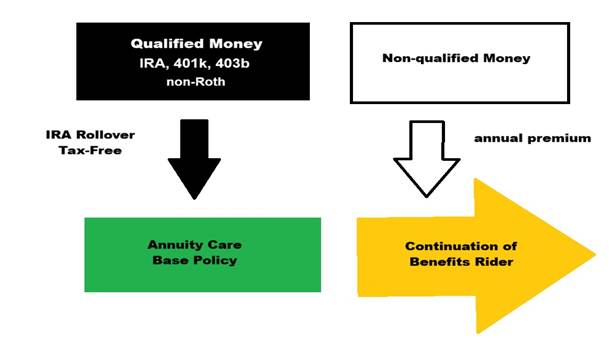

The answer is that we will accept qualified money in the base portion of Annuity Care 1 or Indexed Annuity Care. We cannot accommodate qualified money with Annuity Care 2.

All of this comes with a giant caveat. That money that is rolled into the Annuity Care base annuity will be taxed when distributed (whether it is for long-term care or simply income). If, the client includes the continuation of benefits rider, those monies will be distributed tax-free.

In order to accommodate this, the continuation of benefits rider needs to be funded from nonqualified money (not from the IRA rollover used to fund the Annuity Care product). Here is how it would look”

Let’s talk about the Continuation of Benefits (COB) for a minute. This can either be a finite pool or an unlimited stream of long-term care benefits. It really comes down to what the concern is for the client. A reminder – the continuation of benefits rider will pay TAX-FREE benefits.

In order to make this happen, the premium must be paid from non-qualified money. That can come from any source that is post-tax. So, you could split the IRA into two pieces and use one to fund the base Annuity Care and the other proceeds to fund the COB. As a reminder, since the COB is defined under section 7702b of the Internal Revenue Code as long-term care insurance, that premium may be deductible if the client qualifies.

Effectively, what this strategy is doing is allocating a portion of their qualified money as their long-term care emergency fund which includes a stop-loss position. That stop-loss is what the COB represents.

As with all Care Solutions products, the OneAmerica Financial Care Benefits Concierge is included.

You must be logged in to post a comment.