Last week, I shared information about using qualified money with the Annuity Care products. This week, I am sharing a quick example.

Remember, this strategy employs both the base annuity and the continuation of benefits rider which means that the client needs to be insurable by Annuity Care standards. Remember, we can write up to the age of 85 with the Annuity Care and Indexed Annuity Care products.

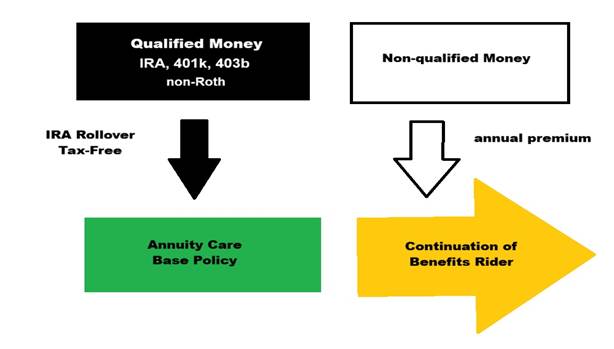

Let’s say that our client is 70 and has an IRA of $465,000. He has other qualified money and invested assets, but this IRA is just hanging out with no real need for income from it (now or in the future). The ideal scenario is to roll it into the Asset Care strategy but he is of the opinion that he can self-fund any need that may come his way.

When you share the strategy of dedicating a pool or resources for a potential LTC situation, he says that this particular IRA will be where he starts. You share the idea of designating that IRA as the resource but putting in a stop-loss position to limit his outflow during a care event. He likes that idea so, you share with him Indexed Annuity Care with a 48 month benefit (24 month COB).

SO, he performs an IRA rollover into Indexed Annuity Care of $409,007 and another $60,000 into a deferred annuity with an income rider to spin off annually $4,907 to fund the COB.

Year over year, the Indexed Annuity Care base will grow (in this case he selected the fixed bucket). And, the COB will grow at a rate of 2% (he elected for a 2% compound inflation on the COB). In 10 years, the annuity value will have grown to $512,277 on a guaranteed basis (which is a minimum guaranteed rate of 2.45%). His long term care pool of resources at this point will exceed $1,000,000.

When a situation arises (let’s say in year 10), he will have $23,479 each month for up to 4 years for long-term care. Remember, the first two years, he is effectively self-funding. Those distributions will be taxed at his ordinary income bracket. Once he exhausts that pool of resources, the benefits from the COB will commence tax-free until it is exhausted.

As a side note, since this is an Annuity Care solution his spouse could be added as an “eligible person” where they could both receive LTC benefits.

And, as with all Care Solutions products, the OneAmerica Financial Care Benefits Concierge is included.

Want more information or ideas?

Give me a shout.

You must be logged in to post a comment.