Let’s take a look at another funding idea this week using nonqualified deferred annuities.

Why do I focus on nonqualified deferred annuities?

Great question grasshopper (summoning Master Po speaking to Caine from the television series Kung Fu) … the reason is that only nonqualified deferred annuities have the ability to transform their gains into tax-free long term care benefits.

As you know, this is possible due to the Pension Protection Act of 2010 and there are very few carriers that offer annuities that meet the PPA requirements.

Keep in mind that these solutions do not simply waive charges, they provide tax-free distributions. And, the tax-free benefits are available for both home care and facility-based services.

So, let’s take a look at an old idea that has come to life recently. That is the idea of a split annuity.

In this instance, rather than a growth and income strategy, we will focus on a growth and protection strategy.

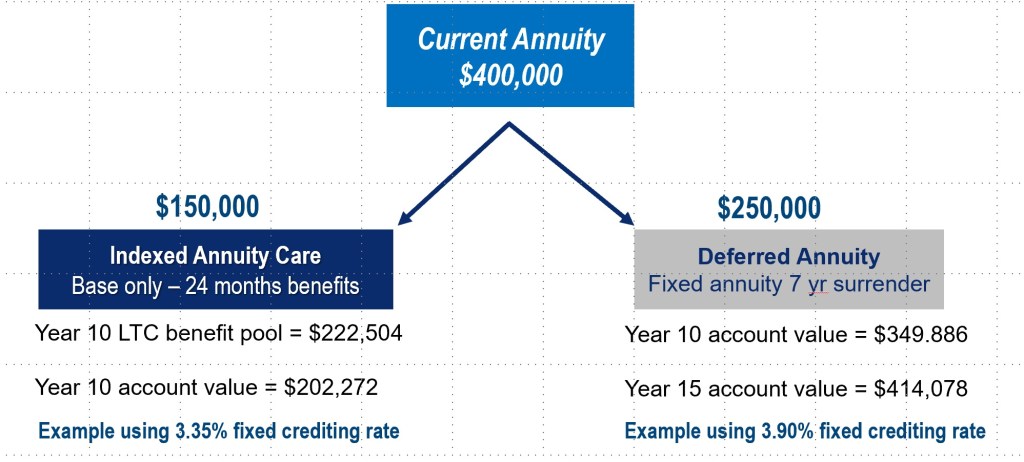

Let’s say we have an existing nonqualified deferred annuity with $400,000 of value, out of surrender, and a client need for long term care. And, let’s say the client wasn’t really convinced that they’d need care but “wanted to hedge their bets” and do a little something to feel better.

So, we split the annuity with $150,000 moving to a base only Annuity Care policy and $250,000 moving to a deferred annuity for growth. Both will grow at the crediting rate associated with that product.

If the “growth” annuity grow annually at a rate of 3.90%, in less than 14 years, it would have a balance in excess of $400,000.

In the case of Annuity Care (I used the fixed account of Indexed Annuity Care), the monthly long term care benefit pool would have increased to $222,254 in year 10 and would continue to accumulate every year.

Do me this favor – contact me with your net annuity case for a client who is 70 or older and has that money earmarked as either “leave on” or “emergency” money. We might be able to create a better solution.

You must be logged in to post a comment.