Last week, I shared an idea using a split annuity to play some long term care defense while recovering the annuity value over time. This week’s variation will be a purely defensive play.

This strategy is made possible by the Pension Protection Act.

As a reminder, in order for an annuity to qualify as a PPA annuity and provide tax-free LTC benefits, there are two basic pieces that need to be present.

- The first part is that the proceeds from the annuity must be available to pay for all levels of care (home-based and facility-based care).

- The next is that in order to qualify for tax-free distributions, the annuity must follow “trigger events” as detailed by the Health Insurance Portability and Accountability Act (HIPAA) which is:

- Inability to perform 2 of 6 activities of daily living, or

- Severe cognitive impairment where supervision is necessary

Back to our discussion of this week’s Split Annuity strategy…

Let’s say we have a nonqualified deferred annuity that is out of surrender and not intended for income. In fact, it was set aside as an emergency fund for a healthcare need. The concern is not at all about growth for this money, it is all about access for a future healthcare need.

In this strategy, what we will do is split the annuity into two pieces.

- One will fund the base Annuity Care policy.

- The other will go into a separate annuity that we will use to fund the continuation of benefits rider.

- That second annuity can be either a Single Premium Immediate Annuity or another deferred annuity where annual distributions will be made.

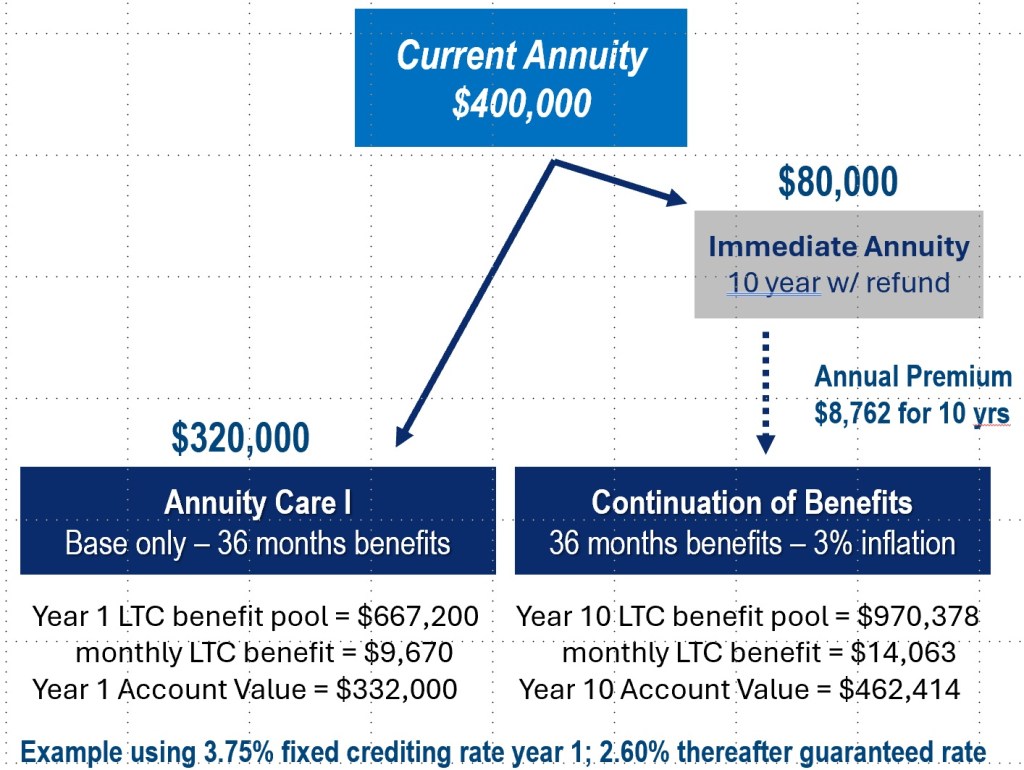

Here is how it would look for a 70 year old female moving $400,000 into the strategy. In this case, we will be using Annuity Care I. (Product availability varies by state, please check with my internal sales partner Justin Fox for product availability.)

1035 exchange A of $320,000 will fund the base Annuity Care I policy; and 1035 Exchange B of $80,000 will fund the premium producing annuity (in this example a SPIA). That SPIA will be designed as a 10 pay with refund producing $8,762 and used to pay the premium for the continuation of benefits (COB) rider.

In this example, the Annuity Care I policy will be a base policy with the COB providing double the base benefits including a 3% annual compound rate. (Keep in mind, we could add a lifetime COB rider.)

What this produces is in year 1 a pool of $667,200 for long term care benefits that can be drawn down at a monthly rate of $9,670 for up 72 months. In 10 years, that pool would have grown to $970,378 with a monthly benefit of $14,063.

If she dies without ever using the policy for long term care benefits, $462,414. Again, the objective of this strategy is not to make her rich, but to keep her from becoming poor.

When distributions are made for long term care services, they are tax free and reduce the account value dollar-for-dollar. Once the base policy has been exhausted, the continuation of benefits rider picks up until it exhausted.

In this case we turned $400,000 into a pool in excess of a million dollars at age 81 when a long term care claim is more likely to occur.

Have questions? Please reach out to either my internal Justin Fox or me.

You must be logged in to post a comment.